Building businesses from the ground up requires intention, and that starts with the tools we use and businesses we support. We don't want to give Bezos or Google any more of our information, ideas, or money, but divesting from Big Tech takes big intentions.

coFLOWco reviews SaaS companies who are doing something innovative without exploiting our data, labor, or our wallets.

We are avid beta testers: we're always on the lookout for the next creator, ed-tech, or community tool to help us find our collective flow.

We amplify business leaders who are committed to improving workflows, creating access, and helping creators, founders, and social impact leaders work more fun.

Consumers drive overall business trends. Solopreneurs and small businesses make up the majority of businesses. Collectively, "We the people" can shift the economy. If you doubt it look at the recent resurgence of unions.

Have an tech product or startup we should know about.

Collective Flow Publishing Co. supports "Social Tech for Good"

Hot Tip: With Heyday, you really can close all of your tabs. No really...you don't need to keep the tabs in your brain open anymore. You're welcome (not that I can take credit).

Rating: I have to turn it up to 11. This may be my favorite app ever.

Why I like it:

I can't oversell this workflow hack enough. I am not being glib when I say I am obsessed.

I beta test the crap out of everything. If only people would pay me! (I heard there's an app for that. It's on my to-do list.)

If I had one productivity tool to use for the rest of my days, and you made me get rid of all my others I would be fine. Heyday is my number one go-to SaaS winner of the year. This may get my vote for the best app ever invented, as long as they keep the features I love.😉

Granted the plug in in chrome is what is making my life easier, but it's the fact that it's working anytime I am behind the scenes. It makes me feel like I have a research assistant, something my neurodivergent brain desperately needed before I found Heyday. Fun facts: I was almost afraid to share this app because it's like my secret weapon/brain hack. And then I was like, that is ridiculous, and also not how I work...at all! I am an over-sharer, especially with great tools and resources. When I find something I love I am a brand ambassador and tell everyone I can about your amazing biz.

Me wanting to keep it for myself tells you just how enamored I am with Heyday XYZ; it was that precious to me when I started using it last summer. I shared about it in the first few issues of the HOT LIST (launched back in December).

I couldn't just tweet about it. My fave tool deserves a full on Em report. So, here my verbose, yet engaging thorough design and user feedback long-form review of Heyday.

Meet Heyday, your research helping hand.

Heyday automatically saves your research, and resurfaces it when you need it.

Our lawyers told us we can’t say that it gives you a photographic memory. ;)

Heyday (originally called Journal app) is a SaaS browser plug-in, desktop, and mobile app that that when installed saves everything you look at and click on. It has a powerful search index; as a researcher and internet spelunker I feel was so needed, with how much Google's sucks these days.

Along the way, they have added some new features like article summaries, youtube video summaries (so rad!) and highlights so share quotes and remember stuff without having to copy/paste to other docs (though, I still do for now).

For a while, these guys started out with a combo of a browser organizer and notion documentation and it had a cool motion visual: every time you opened a new browser window a linear bubble would prompt you to breathe (and it really worked on me since I hold my breath constantly). That said, it took up way too much memory, but was a really nice change from the boring Google search bar.

They moved away from a journal app and embraced the thing they're really good at: saving your content so you can find it later. In previous versions, you could create different views and add documents or notes-like Notion Lite, but the whole experience has been simplified, and while I was hesitant to see features go, they made the right call.

You can grow your body of sources around subjects and themes and assign them "topics" (previous versions called it Spaces, but it's basically the same except simplified for faster, easier assigning/tagging via topic.

The best "new" feature that showed up late in their beta/early in the paid version is this handy reminder when using Google search! You get to see what you already found on the subject. The first time this happened, I think I fainted.🤯

Google something and see what you already found on the subject! Forgot you were already looking at that last week?

Heyday didn't.

How to know if this App is right for you. (This checklist also applies to The HOT LIST, our members-only newsletter created just for creators, founders, and solopreneurs who want all the info and have none of the time.)

When you do research, do you save your deep dives?

Do you look at a variety of sources or always go to the same 3 websites/news outlets?

What defines "content" and how do you track it?

Ever want to share an article your read last month, but you have a more visual memory and can only remember the header image?

Do you save data sets or screenshots and have folders in disarray?

700 tabs every day? Afraid to close them?

Love sorting things into buckets (what I call them) or groups, themes?

Think Google Search sucks now?

Are you a connector with ideas and information, (this is how we build neural pathways and remember/learn things btw), finding the thread and connections between someone's post from today and a tweet from last summer?

Samiur Rahman and Sam DeBrule are super nice and approachable...but also totally buttoned up.

Community: The co-founders and their way of building this product with the community are rad. They have a good tag team thing going, with Sam on community and Samuir on product. They are listening and meeting with those who are highly invested in their beta.

They are into highlighting and connecting creators with a growing Slack. Not super active but not dead and Sam keeps updates around the product coming. It's clear everyone that's a deep fan is rooting for them. The sentiment got more serious since they went to a paid version and the community doubled.

On their Slack, "Every week top creators join our community for AMAs." They past ones are organized and easy to find -how on brand ;). You can read about every creator so far and join their community (if you love the app) here.

Besides the AMAs and Sam's Twitter stream, it's still a nascent, fast-growing group. From like 100 to ~4000 in the few months since I joined.

The shares and posts are getting a bit heavy on bros but I have not even jumped in much yet. For now, I am a lurker.

Note to HQ: Please create community guidelines so that one channel isn't 2 "creators" sharing all their Medium posts. And so you can ensure it's more than a help desk with griping beta testers. Need help? I might know who can help with that. ;)

Follow Sam here for solid creator-economy and tech tweets in storytelling format.

Personally, the workspaces channel don't resonate like they do with the majority of the community. I am old, I have kids. My workspaces are often not my own. People love sharing photos of their home setups and it's sweet to share our "workplaces" but not really relevant to the product and there are probably additional ways to engage with this ND crowd.

Brand Design/Voice: Their new branding is fire! I love the green on twitter-very ownable and unique. Love the hands and color palette. Feels very versatile and fun and just an all-around strong brand ID for a startup that does not feel like everyone else's in SV. Big fan of the lighthearted, personable brand voice. Doesn't feel overly gendered, academic, or SV tech bro.

Performance/ Productivity: When Heyday was still called Journal, it had this awesome feature. When you loaded a new browser page it had nature imagery and encouraged you to breathe. It was awesome BUT ironically, it made my fan go 24/7. For me it was not a deal breaker. I really need a new macbook anyway.

If Heyday could prevent me from still opening 2 dozen tabs, then they’d be brain hackers and I might be scared. They're not magicians.

What the app did do however was prevent me from freaking out if I have to close them all at once, if my computer dies because I forgot to charge it, or if I want to remember that one article about that one thing and cannot remember anything but the source, writer, or imagery.

For my brain, cleaning before starting a new project is not only necessary, but a ritual. Now, I can try and get through all my open work, but if I have to start fresh, I force quit Chrome and voila.

For me productivity in a capitalist sense is NOT the goal. But in a I didn't lose that thing because I forgot where I put it, I do care and HeyDay very much fixes that problem.

Inclusion: Co-founder Samuir is neurodivergent; they created this tool and modified based on how ADHD brains work and because filing your research sucks.

Side Note: Completely off topic, but not for me...I went DEEP on the design studio they hired to do their branding. Evidently, it was the same studio that did Hillary's campaign H➡️. Know what else I found out? The agency is two white guys. Not that their work is not the bomb or notable; it is! But this is your reminder to hire diverse creatives and studios! Especially if your Hillary Clinton, but also if you're a startup. Lift each other's boats!

Challenges:

The features I love in beta are not all carrying over as they shift directions. That said, this is not a problem really. They are focused on doing one thing very well and I would concur that is where they, and most product platforms and SaaS should focus.

The features I love are the part this app saves you from anyway! The tedious tasks of folders and tags and organizing are not necessary for you to find stuff. (I really liked spaces and they just changed that to Topics which I am less jazzed about. The jury is out there but so far their product decisions have been solid.)

I wish I could escape Google’s g.d. grips but the chrome extensions are lifesavers. And Heyday’s hits it out of the park!! They do have them on other search engines, as Fast Co was quick to point out.

NOT to be confused with Heyday.ai which is something else entirely. (Reminder to SaaS founders to do a deep dive on your handles and urls/naming).

I wish I could sync it to Gitbook and Canva like I do Google Docs. THEN I’d really have a record of my brain.

My motives are not always 100% altruistic in promoting new tech platforms and businesses.

With so many new SaaS tools for creators being released daily, there are a lot of opportunities to change tech for the better.

Occasionally when I beta test or dig into a company, I end up finding more synergy. This is the case with Heyday but it is not why I chose to highlight them first.

I chose them because it's coFLOWco's freaking mission:

Our mission* is to achieve equal opportunity and economic empowerment by amplifying the strengths, voices, and creative ideas of diverse leaders.

I chose them because the founders didn't send me an email to eff off because I had some feedback and offered to share it.

HeyDay is truly a game-changer, especially for creators, writers, and educators who love to share knowledge, tools, and tips with their creator communities (like me)! Happy searching.

It’s a relief to know that wherever I talk with others (Slack, email), the notes of our convos or some part of my research will take me less than 5 minutes to find, if that. I don’t need to tag or file it or worry where it lives, but if I do…even better.

For now, I can die happy searching, reading, and jumping around the web with wild abandon till the sun comes up. There's always more to learn...but first, a nap.

In my experience, small business CEOs and founders fall into one of two camps with money. We're either the operations/project management-type, allotting for every dollar, or the creative/strategist-type, worrying less about the price of stickies and more about what's written on them. Depending on the day, you may have to be one or the other.

If you're lucky, you have the cushion to ignore the finance details and stay focused on the big picture. Regardless of your attitude to risk, debt, or your P&L, it's possible you haven't given where you bank or your credit card choices much attention. (Privilege plays its part here, but let's table that...for now.)

Despite what pro-capitalists will tell you, there isn't just one right approach to handle finances, nor is there only one business model you must adhere to. If you consider yourself a social entrepreneur, an anti-racist, sustainability and equity advocate, you already think differently and prioritize social and environmental impact over profit.

To be authentic in your "business for good" leaders must be holistic and transparent with money above all else. Yet, only a fraction of bigger companies voluntarily track EEOC data. Transparency is hardly their strong suit.

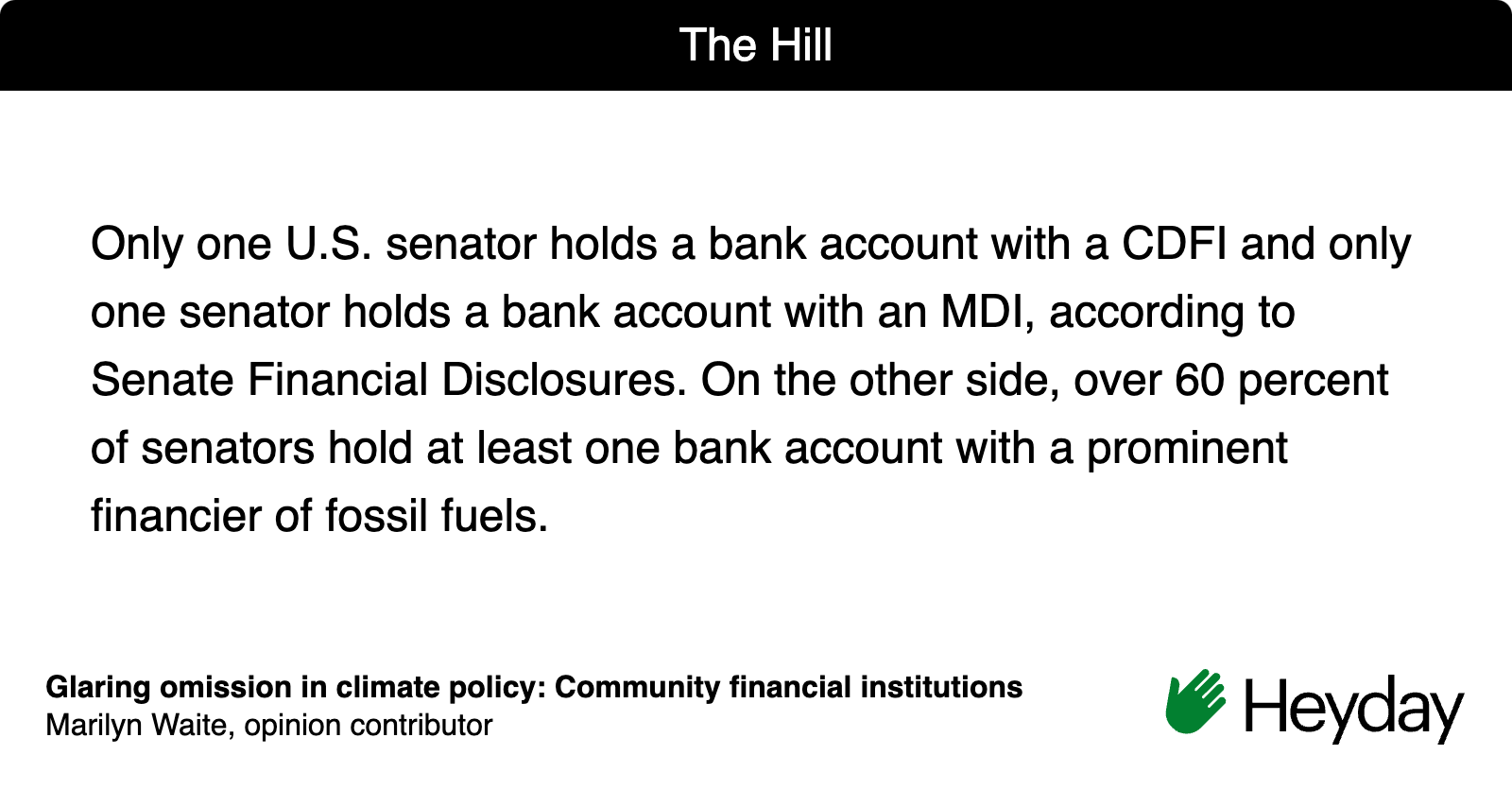

What drives your choice in where you bank? Here is is one area everyone can affect the global economic system. We must literally put our money where our mouths are, and move it to small, local, independent banks.

In this Inflation Nation, we have to look beyond interest rates when deciding which bank to deposit checks and run payroll from. Don't be fooled by headlines that "small banks are failing." Your money is insured up to $250k, and your safer at a local community or black owned bank-and better yet, at a credit union.

Does it matter who holds your hard-earned revenue? Absolutely. This should be your first big money move as a founder after you incorporate or set up your LLC.

Why? Because, climate change.

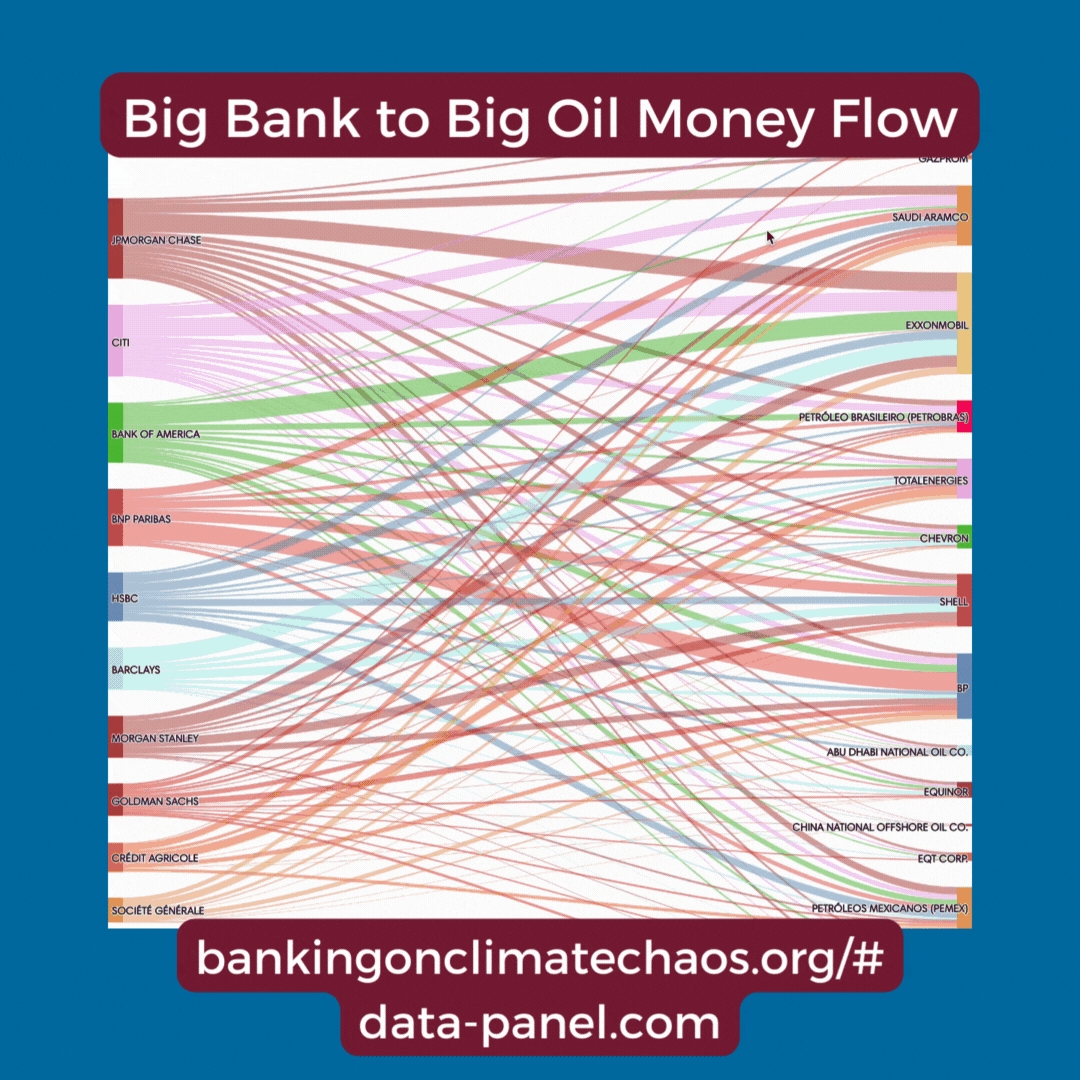

“In the six years since the adoption of the Paris Agreement, the world’s 60 largest private sector banks financed fossil fuels with USD $4.6 trillion.”

More reasons I choose to bank as much as possible with Local Banks and Credit Unions (CU's) include:

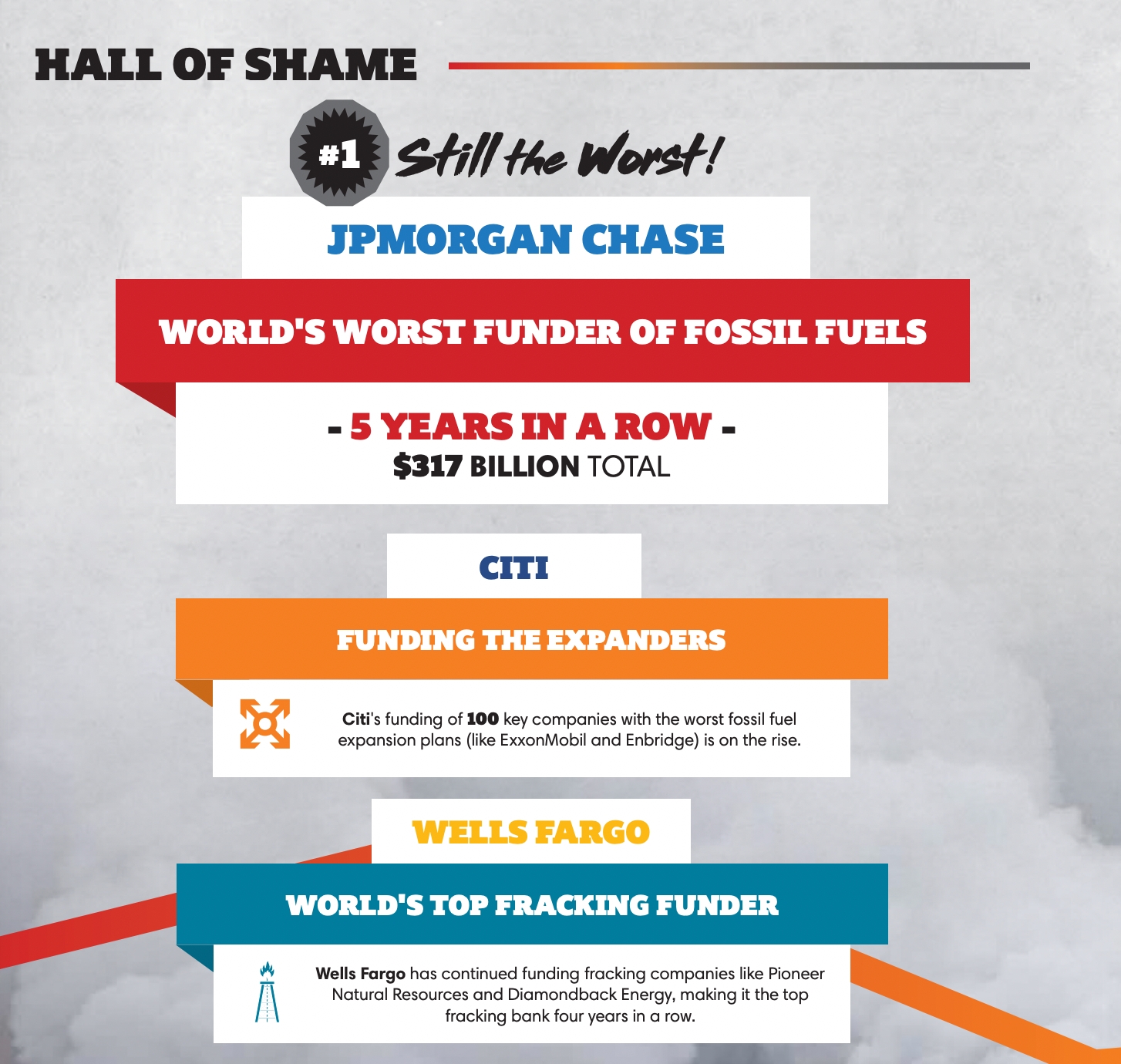

Local Banks and CU’s DO NOT fund big oil.

Local Banks and CU’s DO NOT kowtow to conservatives.

Local Banks and CU’s DO NOT use my money as a loan for the 1%.

Local Banks and CU’s DO NOT hurt the climate.

Who do Big Banks love help out first in an economic crisis? The little guys? We wish!

Who does the government send money to first in an economic crisis? Big Banks.

Need another reason to bank small? Big Banks do NOT care about small businesses or solopreneurs.

Local Banks and CU’s saved small businesses during the Pandemic and until their help, small businesses received virtually zero federal money from the CARES Act and PPP.

"ProPublica found 270 taxpayers who collectively disclosed $5.7 billion in income, according to their previous tax return, but who were able to deploy deductions at such a massive scale that they qualified for stimulus checks. All listed negative net incomes on tax returns."

The wealthiest Americans reported negative income (pure B.S. tax razzle dazzle) which led to more negative outcomes for small businesses, negative impacts on our planet, and greater wealth inequality. Federal money was passed back and forth through Big Banks, and they keep on doing it now.

Our representatives prefer big banks with consolidated power, despite the incredible impact credit unions and local banks can have for small businesses.

If the companies who invest and bank with the places that support fossil fuels, they are creating a bigger opportunity for banks to fund and loan to big oil.

It's not just your banking choices that impact carbon emissions. It's companies you use everyday to get work done in a capitalist society. Tech Companies are the biggest contributors to climate change, but not necessarily with their own operations.

“For some of the world’s largest companies, including Alphabet, Meta, Microsoft, and Salesforce, their cash and investments are their largest source of emissions. In fact, for Alphabet, Meta, and PayPal, the emissions generated by their cash and investments (financed emissions) exceed all their other emissions combined.

Linkedin wants me (all of us) to buy Ads to boost my post. Somehow, most of my Big Tech, Big Bank, and Big Oil posts get 1/4 of the impressions (I can't imagine why?!) As a result my engagement goes down after each one for weeks till I build back up with more banal content. Meanwhile they use my money to loan to a bank like Bank of America who loans it to Exxon. Sweet, right? FML.

"Researchers selected the companies featured in this report to illuminate the magnitude of corporate cash and investment emissions and to highlight how companies’ climate accomplishments are being undermined by a misaligned financial system that is channeling hundreds of billions of corporate U.S. dollars into the carbon-intensive sectors driving the climate crisis.

...A comprehensive breakdown of the methodology used to calculate the emissions each company’s banking practices generate can be found in the Appendix."

“Banks play a foundational role determining our climate and economic future by taking short-term money and investing it in long-term infrastructure. Presently, too much of that infrastructure is furthering the climate crisis. The longer this situation persists, the more challenging it becomes to achieve global climate goals. As a result, by passively enabling their cash and investments to finance carbon-intensive sectors and infrastructure, companies have been unintentionally funding a future they are working tirelessly to avoid.

Conventional banking has not worked for businesses led by anyone other than those led by white men. PPP loans stats proved this beyond a shadow of a doubt. By design, using Big Banks also contributes to systemic racism and wealth inequality because you are supporting inequitable institutions and because climate change and pollution impacts Black and Brown communities much more than white communities.

But, we know this doesn't work for the 98% of white women and 99.9% of Black women who do NOT get VC funding. Not only are they looking at speed to get money to those who need it, using local banks and credit unions. They're exploring a different lending model based on character, not Credit Scores, another racist and sexist part of finance.

“We’re going to be burning money just to adapt...Just the status quo is going to start costing us more.”

Six banks – Bank of America, JP Morgan Chase, BNP Paribas, SunTrust, US Bank, and Wells Fargo – have provided major financing to the two main private prison companies, helping them expand, diversify the ways they profit from imprisoning people, and lobby for harsher criminal penalties and stricter enforcement of immigration laws.

Being poor is g.d. expensive. Knowing this doesn't do much for poor people who still have roadblocks keeping them broke and oppressed.

"Those with low- and moderate-incomes face numerous barriers to accessing regulated, low-cost, financial services that could improve their financial footing."

Predatory lending practices ensure that poor people, (1/2 are people of color) pay BIG TIME in some way, especially with banking access.

giving loans people can't afford (especially before the 2008 housing bubble burst)

late fees for credit cards, SaaS platforms, mobile phones

reconnection/ reinstatement fees

fees for overdrafts.

PLEASE explain to me how this system has been in place so long? Only in the last decade is Congress even talking about this.

Why do those who run out of money get charged more money to then be further out of money?

Example: My credit card autopay was declined. My bank (a local credit union mind you) charged me $10 for the 1st attempt to pay, $10 for the second...before I even knew anything was amiss. When I had more money in my account, those fees were either covered or only $2, but when I am month to month, thanks to clients Net-45 and paying my people on time, I am out fees constantly. Society shames people who can't pay bills on time as if we don't want to or have a mental deficit that means we are less worthy, and charges us a tax for our "stupidity" or inability to make things work. Of course, the opposite is true. Their stupidity led to the belief that poor = lazy or incompetent. We are smarter and more resourceful with money. We understand The Economy better than a NY Times Economy "expert." Being wealthy does not make you wiser, but it does make you healthier.

If people can't get approved for traditional banking, they remain unbanked or underbanked.

unbanked: no member of the household has a checking or savings account

Low credit scores and low cash flow forced the unbanked into AFS, alternative financial services (AFS) which include:

underbanked: someone in the household has an account, but they still rely on high-cost AFS

check cashing, payday lending

pawn shop loans, rent-to-own

Buy now, pay later (BNPL)

Big banks are incentivised to be predatory because it's more lucrative. Poor customers pay fees instead of building up a savings, (with AFS options charging up to 400% APR.)

"In 2017, the unbanked and underbanked LMI populations, and those with little or no credit history, spent more than $173 billion in fees and interest for AFS."

Americans unbanked and underbanked include:

63 million adults

47% Black households (nearly 1/2!)

43% Latina households

More than half (54%) of [those in poverty] are people of color.

Almost 1/3rd (96 million) of adults live on income of 200% below the federal poverty guideline (which is not even a good guide. It's an outdated metric never intended as a long term usage and keeps people working at jobs with unlivable wages.

The above May 2021 report "follows up the Asset Building Policy Network’s (ABPN) 2014 Banking in Color" and looks into the experiences within LMI communities of color with financial institutions.

Not surprisingly this is terrible for your health, where fringe loans were "associated with 38% higher prevalence of poor or fair health, while being unbanked (not having one’s own bank account)" increased the prevalence of poor/fair health by 17%.

More than this, the United Nations and World Bank predict that there will be between 140 and 200 million climate refugees by 2050 as continued warming leads to increasingly frequent and intense natural disasters.

A recent report from the APA (American Psychological Association) published in October 2022 shows just how much of a wreck our country is financially.

"Money is causing stress for 72% of Americans," and this doesn't account for those without digital access. The virtual Harris Poll survey was conducted in English and Spanish on behalf of the APA.

Americans who are already the most underbanked and underfunded, who don't speak English or Spanish, or who have no wifi were left out. Missing huge swaths of the population relevant to this data is why we can't have nice things. 72% is probably low.

Per a different study from Bank Rate & Psych Central, "42% of U.S. adults say that money negatively impacts their mental health."

If we continue to claim that Big Banks (fueled by Big Tech, Big Oil, and an even bigger military budget) can solve our financial woes, we are ignoring more than one elephant in the room.

We cannot "build business for good" if we ignore the negative social and emotional impacts that a lack of banking and finance options can cause. As the same study, whose takeaways feel suspiciously conservative observed,

"Everything from dealing with debt to managing money was linked to a decline in psychological well-being, leading to such outcomes as anxiety, stress, worrisome thoughts, loss of sleep and depression."

A lot, actually, but not through less Starbucks or saving more. Systemic economic inequality cannot be fixed overnight. Remember how Bernie was always ranting about "breaking up the banks"? This is why.

Still, there are policies you can support and money moves you can make IF you have some, especially if you are a small business owner and social entrepreneur.

"Conventional banking hasn't worked for businesses owned by people of color. But a new network is designed to get money flowing fairly to BIPOC economies."

Why? Credit scores are racist.

This makes it easier for Big Banks to be racist when it comes to lending for small businesses and home mortgages.

While banks pay out a few hundred million to make racial discrimination lawsuits disappear, we need systemic changes to the way banks finance communities already impacted more by pollution and climate change. It predicates the need to change not only using big banks, but the lending practices themselves that still impact Black and Latina families at credit unions (by far less).

Where can you bank instead?

If you care about the climate and systemic wealth inequalities due to systemic racism...move your money elsewhere and dig in DEEP to what the companies you support are doing with your money.

Seek alternative financing, avoid debt, especially VC money that forces a quick exit. Keep your budgets and compensation structures transparent. Prioritize people and planet over profit by taking your money out of Big Banks and investing more in Black businesses and keeping your money in Black-owned banks and coops.

Founders make a million decisions all day, often stretching a bank accounts and our bodies beyond capacity. One decision I have always felt great about? Being a member of a local Credit Union, and not just a consumer, feels good, confident I am doing business differently where it starts: money. We can't stop capitalism, but we can stop financing is at scale. Bank small; Collectively our small moves can make a big impact!

The report "Banking on Climate Crisis, Fossil Fuel Finance report, 2021" shows how U.S. banks are tiny in comparison to other state banks like China but "they disproportionately ." Not only that, Citibank is just one example of these Big Banks seeking investments to expand extracting fossil fuels, increasing petroleum production.

Big Banks to their wealthiest clients and large businesses through the Paycheck Protection Program.

It wasn’t until were added to the Small Business Administration’s roster of financial institutions that the loans flowed to those in most need. The importance of the community-focused lenders such as community development financial institutions (CDFIs) became so apparent that when the PPP portal reopened at the beginning of 2021, CDFIs were granted an exclusive access period. As of June 2021, these institutions have deployed close to . – - The Hill

They also flagrantly discriminate with lending and racial profile those who need their money fast. Big banks have a big racism problem which harms loyal customers like

Despite large U.S. banks being tiny compared to other global banks, such as those headquartered in China, they disproportionately . It was these same banks that to their wealthiest clients and large businesses through the Paycheck Protection Program that emerged to help businesses sustain the economy.

What's worse? Only SOME of them returned the money and acknowledged the error, when the media called it out.

That means for a company like Microsoft, in 2021 the emissions generated by the company’s $130 billion in cash and investments were comparable to the cumulative emissions generated by the manufacturing, transporting, and use of every Microsoft product in the world.”

Let's consider how our individual money impacts this . Example, I pay $30/month to LinkedIn, owned by Microsoft. I do so through the App store so no doubt Apple takes 30%. For $20, I get shadow banned whenever I try and make a living or post about work.

"So you have a big idea, you start your business and you want to take this fledgeling product to the next level. Typically, you’d go through a “standard” funding journey. First, you’d turn to your closest allies for the friends-and-family round where they can support you before you’re able to prove yourself to creditors or funders. After that, you either turn to the traditional financial system for a loan, or to venture capital firms for backing." ––

In addition to Common Future, and predatory lending on Black and Brown communities. It bears repeating here that a lack of inclusive financing is one more reason to skip these banks. Climate, racial, economic, and gender are inextricably linked.

It is not going to get better unless people take bigger moves to halt climate change. As they point out in

Fringe borrowing, as noted in "Health Affairs" does not require credit checks...which immediately places the person borrowing in a precarious position, used for an emergency that quickly balloons when that loan's APR is 400-600% of the balance.

, the solution is not to fix the impacts from poor health but to address systemic inequality by "expanding social welfare programs and labor protections would address the root causes of the use of fringe services and advance health equity."

Community banks:

It's not easy! For more on why it's hard to escape Big Banks, read the report below: (Action Center on Race and the Economy)

Ask anyone who has ever struggled to pay rent or build a business. Money is stressful and emotional. Pretending it doesn't exist is what the Big Banks are doing with climate change. We can do better than throwing up our hands. Make a plan at . Find your bank, set a date, and start moving your money. Not ready yet? You can sign up for reminders to do it in the future. What will your story be?